What are Anti-dilution Provisions?

For early-stage companies, convertible instruments offer several advantages over conventional debt or common equity.[1] However, because start-up companies change their capital structure so often, investors with convertible instruments are particularly vulnerable to changes in the value of their investment. Anti-dilution provisions are a commonly required protection for investors in early-stage companies. The purpose of anti-dilution provisions is to ensure that a convertible instrument retains its economic value to an investor in the event the company changes its capital structure. If the company splits its shares, for example, an investor holding a convertible preferred share should be able to convert his shares and receive the same proportion of the company as he would have before the split happened. That is an example of a corporate structural anti-dilution provision, the other type of provision is the price-protection anti-dilution provision.[2] Corporate structural anti-dilution provisions Corporate structural anti-dilution provisions ensure that the investor receives the same number of common shares at the same conversion price as he would have if a change to the corporation had not occurred. Common triggers include dividends, division or consolidation of common shares, amalgamation, arrangements, reorganization or recapitalization.[3] Price protection anti-dilution provisions Price protection anti-dilution provisions are designed to adjust the conversion price of the investor’s instrument to align with any new issuances of the companies securities. Generally speaking, these are triggered only when new securities are issued at a price below the investor’s conversion price (“down-round financing”). [4] Common triggers include the issuance of common shares, issuance of options and other convertible securities, or changes in terms of options and other convertible securities. [5] Adjustments to the conversion price are usually calculated in one of three ways:

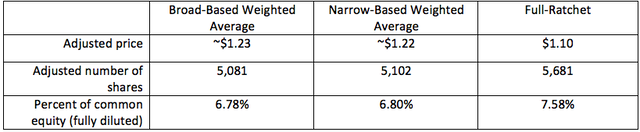

Generally, a full-ratchet method offers the strongest protection to the investor allowing him to receive the lowest conversion price available and a proportionately higher number of shares. To see how that works consider the example below. A company has 50,000 common shares outstanding, and an additional 10,000 common shares issuable on conversion of preferred equity. An early investor has a right to convert his preferred shares into 5,000 common shares at a conversion price of $1.25 per common share. The company subsequently issues 50,000 common shares in a private placement at a price of $1.10 per common share. The investor's preferred shares contain anti-dilution provisions that are triggered by the issuance of new common shares. As the above table indicates, the impact of the price-protection mechanism matters a lot. Agreeing to anti-dilution provisions without considering the overall dilutive effect of such provisions could have serious consequences for holders of common shares (including managers or key employees). Investors with bargaining power over a company will be able to extract stronger anti-dilution protections. Given the sizeable effect these provisions have on the company’s ability to attract future investors and potential dilution to common shareholders without these protections, companies should seek to limit or scale back the strength of anti-dilution provisions. How can a company limit the severity of anti-dilution provisions? Companies should be aware of the consequences of overly-strong anti-dilution protection given to early investors. When negotiating convertible instruments there are several ways a company can limit the severity of anti-dilution provisions.

__________________________ [1] Bryce C. Tingle, Start-up and Growth Companies in Canada: A Guide to Legal and Business Practices, 3rd ed (Canada: LexisNexis Canada Inc, 2018) at p 85 [Tingle]. [2] Thomson Reuters: Practical Law Canada Corporate & Securities, Preferred Share Provisions: Conversion Privileges and Anti-Dilution Protection, s 3.6 “Adjustment to Conversion Price and Number of Conversion Shares” (Retrieved on October 7, 2020) [Thomson Reuters]. [3] Thomson Reuters, notes to ss 3.6(e) and (f). [4] An investor might demand adjustment to their conversion price even if the price of new securities is higher than their conversion price, but lower than fair market value. Companies should do what they can to negotiate out of this trigger as it limits flexibility in future financing rounds (see Thomson Reuters, notes to s 3.6(a)). [5] Thomson Reuters, notes to s 3.6(a) and (d). [6] Tingle at p 359. [7] Tingle at p 359; see also Thomson Reuters, notes to s 3.6. [8] Thomson Reuters, notes to s 3.6(g). [9] Thomson Reuters, notes to s 3.6.

0 Comments

Leave a Reply. |

BVC BlogsBlog posts are by students at the Business Venture Clinic. Student bios appear under each post. Categories

All

Archives

May 2024

|

RSS Feed

RSS Feed